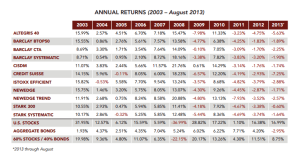

15.EUROPEAN UNION OF NONSENSE

Back in January of 2018, European Union (EU) legislators thought that it would be a good idea to defend european small investors, like me, from the big “greedy” financial corporations that want to take it all.

So they created the Key Information Documents (KIDs) for Packaged Retail and Insurance-based Investment Products (PRIIPs), which is a document that explains and help investors to understand and compare the key features, risk, rewards and costs of different PRIIPs, through access to a short and consumer-friendly leaflet.

This was a really good idea, everything that helps investors to make ponderate and wise decisions is great, because in the investing world every decision comes with doubts and uncertainties, therefore better information and an easy way of visual comparison is a very smart idea.

For US ETFs this meant they would require KIDs for trading in the EU space and that moment was when great initial ideas become shitless.

The major ETFs issuers, BlackRock , Vanguard, SPDR, Invesco, among others, decided that they would not offer KIDs of their US domiciled ETFs, meaning retail investors in Europe were immediately cut off of buying it. At least that was my broker’s case. There are brokers in Europe that still allow US domiciled ETFs negotiation, but in the eyes of EU regulation it should be considered an illegality and so I didn’t even bother to look for another one.

When I understood what was going on I went mad because US ETFs were my entire portfolio.

I sent an email to one of the big four ETF issuers asking when would they liberate KIDs for their US products in Europe and it was when I was informed they wouldn’t release any KID, instead I was advised to look for their EU domiciled ETFs because there were already KIDs available for them.

EU ETFs market is just starting when compared to the US. They lack in sector diversification, value and volume but it was an option, my only option. Then I remembered that EU ETFs have a great plus over US ones, they don’t distribute dividends. Instead they accumulate those dividends making them more tax efficient.

Like a great philosopher called Brian once said: “Always look on the bright side of life” and I did just that, I started conceiving a new portfolio with european domiciled ETFs.

First I thought of my main rules that would shape my new portfolio which were:

- Diversification and allocation – it should replicate my US original ETFs portfolio, therethrough I wanted to have the same asset classes, allocated in equal proportions to maintain similar risk/reward ratio;

- Accumulation – Since it’s allowed in EU to have ETFs that don’t distribute dividends it was no-brainer to go with them, after all they are much more fiscal efficient;

- Euro hedge currency ETFs – Because it’s my daily currency it’s simpler to use it, so for a little higher expensive ratio I’ll get less worries about USD/EUR pair fluctuations or the need to have some kind of hedge, which also costs money.

- Expensive ratio – Less the better.

These were the main rules to reshape my portfolio, therefore I started studying about European ETFs, trying to make some good of this nonsense.

Follow @TridionTrader