8.SIDEWAYS

Last two years have been hard, my portfolio has been flat. Sideways it seems, like in the movie this could be my history of a disillusioned man in his forties, going bald and still dreaming of moving into the investment industry or simply getting rich. At least I shall not drink my best wine in a Mcdonald’s cup. Sad that was, Mr. Giamatti.

Nevertheless, I agree that being middle class sucks, sometimes you do not have time to meet your obligation even more to read, write or think. When you mix middle class and investments your thoughts become blur and that is a sweet spot for mistakes. It is where you make dumb decisions like sell a bottom or buy a top. Or even sell everything and start all over again, thinking “this time I will make it perfect”.

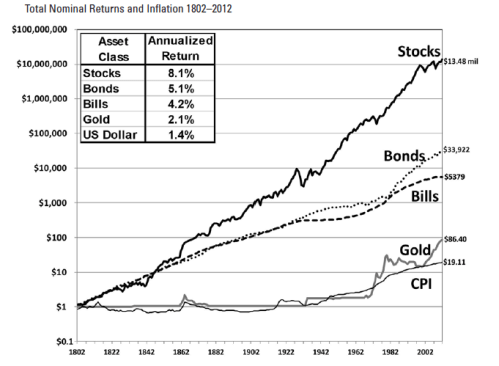

Perfection is something that does not exist, even in upper classes, after all nobody is really normal and we all live with a odd self inside, which made me realize that I should embrace my imperfect portfolio and accepted that will be ruffled times. But guess what? Fewer returns today means greater returns in the future, providing that society and economics continue very similar to last century, which I think it will because people are people, even if today it seems the world will implode at any second.

So if in the future the probability of having higher returns is great, there is only one thing to do that is to putt more money to work. That was exactly what I have done in last market correction. When some of my equities ETFs went under the 30 RSI weekly chart, I bought some more. Although I did not have the courage to go the full monty because I think it is pretty clear that we are relatively advanced in the economic cycle and we should proceed with caution.

So far so good. It seems like my portfolio is giving back some of the return that I did not get in last two years.

In 2017, assets had a good run but EUR appreciation against USD took almost all off my returns. Remember that my assets are USD ETFs and I live in a Eurozone country, so I ended 2017 with a mere return of 0.98%.

In 2018, although last trimester was a value killer, because of my USD based currency portfolio it was not so bad and I closed the year with negative return of 3.97%.

I guess this is what happens when you own all the market and all the global assets, sometimes you get dragged others you get lifted.

Since inception these have been my after-tax rate of return:

This portfolio was design to have an annual return of 10% and last two years it has been lagging. I am confident that in the future it will pick up the pace.

Follow @TridionTrader